No Cold Turkey

- Extraordinary rally in risk markets over the month

- Equities look vulnerable to profit-taking

- Complacency is evident in the equity market with VIX at a 3-year low

- US 10-year bond yield looks to have bottomed out ahead of Treasury auctions this coming week

- German budget is in disarray - eurozone growth at risk

The financial markets have maintained their recent upward run, which has been fueled by a stream of seemingly positive developments that have boosted equities and high-yield bonds. However, we caution against the current wave of optimism, which could face a sharp reversal if the widely anticipated gentle economic deceleration fails to materialise.

The markets appear to have largely shrugged off developments that undermine the soft landing narrative. The recently published Federal Reserve minutes reveal a central bank that expects interest rates to remain high, with the inflation trajectory still fraught with uncertainties.

Contrary to their typical contrarian stance, even the usually cautious investors are seeing merit in the prevailing market uptrend. According to Nicolas le Roux of US Group AG, Commodity Trading Advisor funds, known for their counterbalancing role during asset rallies, have invested more than $60 billion in global equities in the past fortnight.

The upward drift in long-term inflation expectations among households has added to the Fed’s concerns. Notably, the final October figures from the University of Michigan's survey of consumer sentiment indicate that the 10-year inflation forecast has climbed to 3.2%, marking an 11-year peak. Moreover, the short-term, 12-month inflation outlook has surged to a seven-month high of 4.5%.

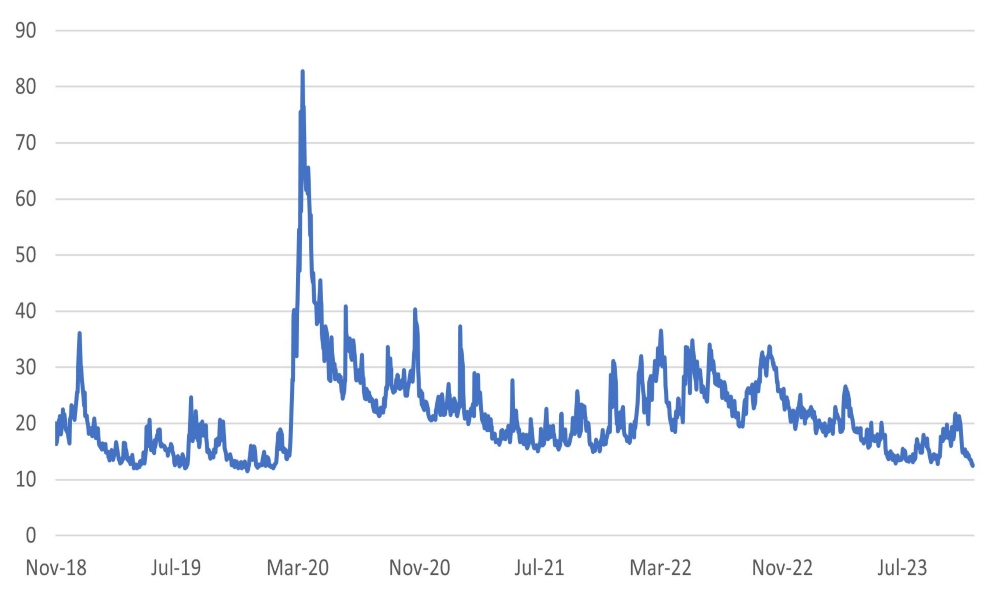

Interestingly, while inflation keeps policymakers and investors on their toes, complacency appears to have crept into the markets. The VIX index, a barometer of US equity market volatility, has dipped to its lowest since January 2020. This has coincided with a significant influx of mutual fund investments into the equity market, totalling $40 billion over the two weeks leading up to 21st November. This represents 28% of the year-to-date total, potentially overstating the market's positive performance

Chart 1: VIX index – a measure of US equity market volatility – drops to its lowest since January 2020

Source: Bloomberg

Source: Bloomberg

Equity markets – a potential reversal on cards?

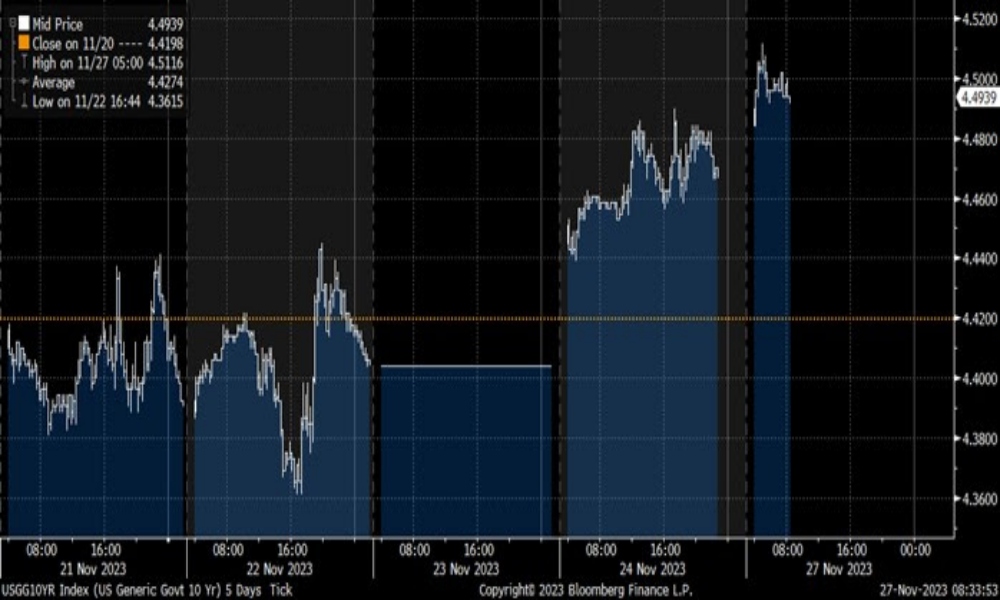

Recent optimism aside, the equity markets face a potential reversal of some of the recent supportive positives in the coming days. The US 10 year may have reached the limit of its rally. Late last week, the US 10-year bond yield started to drift higher. The bond market will be challenged in the coming days by a heavy load of Treasury auctions; on 27th November the Treasury will sell $54 billion of 2-year notes and $55 billion of 5-year notes. On 28th November the Treasury will sell $39 billion of 7-year notes.

Fed Chair Jerome Powell is due to speak this week ahead of the blackout period for the 13 December FOMC meeting. He may allude to the manner in which the markets have given back 60% of their previous tightening since July. Remember commentators had previously argued that the Fed didn’t need to raise rates still further as the market had done to the tightening for them through higher long-term interest rates and wider spreads.

Bond yield reversal evident

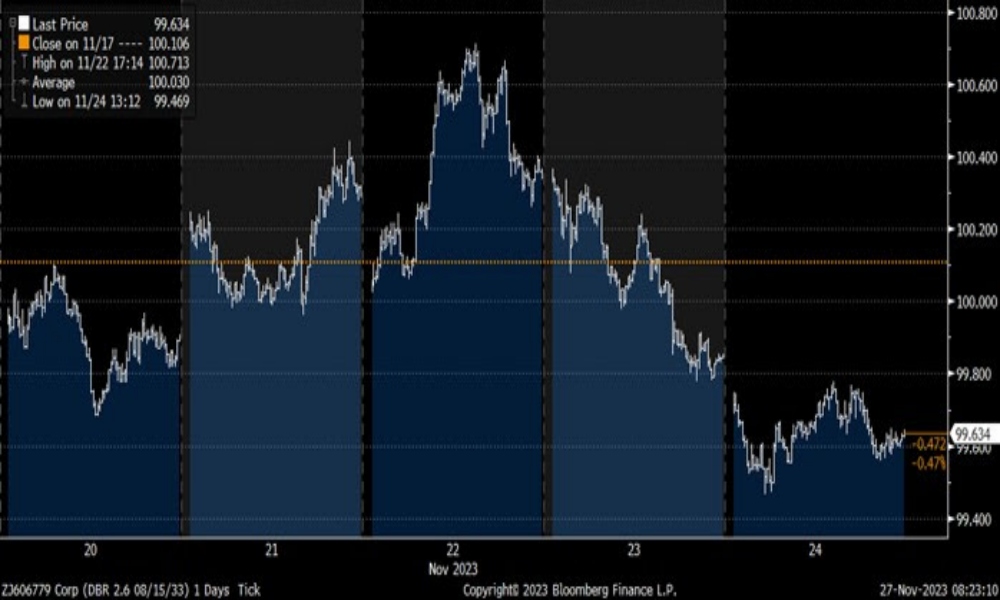

While equity markets have rallied, bond markets have struggled to keep pace. Global bond markets had a testing time last week, which serves as a stark reminder of the challenges posed by the accumulated burden of unsustainable sovereign debt. European bond markets, in particular, felt the impact, with bond prices dropping and yields climbing following a decision by a German court to suspend a constitutional debt brake for the fourth consecutive year.

Chart 2: Intraday US 10-year yield – yields pick up from their lows and threaten the equity market rally

Source: Bloomberg

German government’s predicament – a lesson for the US?

The German government's pledge to adhere to a debt ceiling was a key factor in containing the rise in eurozone bond yields. However, undermining this commitment was the court’s direction to the government to retroactively include at least €37 billion of off-budget expenditures, primarily related to subsidies aimed at mitigating the surge in energy costs following the Russian invasion of Ukraine.

The court's ruling has significant implications, particularly as it pertains to previous governmental spending programmes that were not traditionally factored into budgetary considerations. With the altered dynamics of government expenditures, Germany now faces the prospect of curtailing various planned spending initiatives. This fiscal tightening will likely dampen GDP growth, with some economists projecting a potential contraction of 0.5% in the coming year's economic output.

Chart 3: 10-year German bund price

Source: Bloomberg,

The criticism aimed at the German government often overlooks the broader fiscal realities and is not entirely justified. Suggesting that governments should continue spending without restraint is a flawed strategy. There’s no one-size-fits-all approach and it paints a somewhat misleading picture when some analysts cite the U.S. Inflation Reduction Act as a paragon of fiscal management. While the U.S. administration's expenditure on renewable energy and generous financial incentives might be popular, they are also contributing to an economy increasingly reliant on debt and foreign borrowing. A projected budget deficit amounting to 8% of GDP, coupled with a government debt-to-GDP ratio soaring to a projected 135%, should not be viewed favourably. Sustainable financial governance isn't akin to possessing an endlessly forgiving credit card. Germany's recent experience is a testament to this, and it serves as a cautionary example for the United States, which appears to be treading a similar path.

Copyright © The Global CIO Office, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.